A few years ago I first heard of a new breed of automated investing services, what those in the financial media like to call robo-advisors.

Automated investing services have made investing more accessible to the average investor. It allows a regular Joe like myself to invest in a way that’s based on sound investing theory, that is typically lower cost than a traditional financial advisor, and that is highly diversified and suited to my level of risk tolerance. It’s a set-it and forget it investing program for the rest of us.

![]() I’ve reviewed quite a few robo-advisors on this site, and one of the absolute best automated investing services in my opinion is Wealthfront. Not only are they one of the fastest growing and most respected automated investing services, but they also were among the most affordable. You can find my full Wealthfront review here.

I’ve reviewed quite a few robo-advisors on this site, and one of the absolute best automated investing services in my opinion is Wealthfront. Not only are they one of the fastest growing and most respected automated investing services, but they also were among the most affordable. You can find my full Wealthfront review here.

The only sticking point I’ve had in recommending them to newer investors was the fact that you had to have a relatively high initial deposit and minimum account balance of $5000 when opening a new account. While that isn’t going to be a deal breaker for many, for those just getting started out who don’t have a lot to invest, it might be.

This month Wealthfront wiped out those concerns by getting rid of their $5000 minimum account balance, and instituting a new low $500 minimum account balance!

Sign up for Wealthfront via this exclusive Bible Money Matters link to get $5,000 managed for free:

Sign up for Wealthfront and get $5,000 managed for free

Quick Navigation

Wealthfront’s New $500 Account Minimum

The account minimums are changing for Wealthfront.

So to open an account, you’ll need a minimum of $500. Why not open a new account with $500, and then setup automatic deposits to fully fund your Roth IRA by the end of the year ($6000 for 2019)?

There is also a minimum withdrawal of $250, and you can’t withdraw below the new account minimum of $500. If you withdraw all of your funds it will transfer your money and close your account for you, with no exit fees.

Wealthfront Fees (And 2 Ways To Save Even More)

It’s great news that the account minimum has dropped, but what are the fees that you’ll pay to use the Wealthfront investment service? If your assets in the account are less than $5,000 there are no fees at all if you sign up through our link. Above $5,000, there is a 0.25% annual fee on the assets above that amount.

The Nuts & Bolts Of Using Wealthfront

Wealthfront was founded in 2008, and launched it’s online investment advisory service in December of 2011. Since then they’ve grown rapidly to the point where they now have in excess of $12 billion under management.

So how do they determine what you’ll be invested in when you sign up? First, you’ll have to answer some questions on a brief questionnaire that will tell them the basics like your income, investing horizon and level of risk you’re comfortable with. Then they’ll assign a portfolio based on your answers (that you can modify if you want).

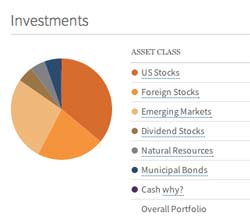

Wealthfront portfolios are based on a mix of 11 asset classes that includes both U.S. and international stocks and bonds. They invest mainly via the following ETFs, although that is subject to change.

Wealthfront portfolios are based on a mix of 11 asset classes that includes both U.S. and international stocks and bonds. They invest mainly via the following ETFs, although that is subject to change.

- U.S. Stocks (VTI)

- Foreign Stocks (VEA)

- Emerging Markets (VWO)

- Real Estate (VNQ)

- Dividend Stocks (VIG)

- US Government Bonds

- Corporate Bonds (LQD)

- Emerging Market Bonds (EMB)

- Municipal Bonds (MUB)

- Corporate Bonds (LQD)

- US TIPS (SCHP)

- Natural Resources (XLE)

Your Wealthfront account holdings will vary depending on whether you have a taxable or tax advantaged account. Wealthfront will give you the most tax efficient holdings for your situation.

Here’s an introduction video from Wealthfront that talks about what they do.

What Kind Of Accounts Can You Open?

Available account options with Wealthfront include:

- Standard taxable account

- Joint investment account

- Trust account

- Traditional IRA

- Roth IRA

- SEP-IRA

- 529 College Savings Program

Free Automated Financial Planner

In December of 2018 Wealthfront launched a new free automated financial planning experience for their clients, to help them better plan for their financial future.

The financial planning tools connect to your existing financial accounts in a few minutes, and then by tracking your actual spending and saving patterns to help you figure out how your financial future may look.

It helps you to figure out how much you need to save now to reach your future goals, and helps you to determine if you’ll be able to live the same lifestyle you live now, in retirement.

Their tools helps take the guesswork out of figuring out if your hoped for future is even attainable based on your current spending and saving patterns. It helps you take a look at “what-if” scenarios, and help you figure out what the impact of a raise at work, or saving more every month might be.

This automated advisor is your personal financial planner, but without the need for a bi-annual meeting at an expensive office with a planner that hardly pays attention to your needs.

Wealthfront – Lower Minimums Should Bring More Beginning Investors

When I first reviewed Wealthfront a few months ago, I talked about how I thought they were a great service. They have an easy to use site, a proven investment strategy, low costs and a strong set of investing tools.

The only people I couldn’t truly recommend them to were beginning investors, because they had a $5000 minimum to open an account.

Now that they’ve dropped the account minimum to only $500, I can safely recommend them to everyone as an easy place to start investing. Not only will you get a highly diversified portfolio, but you’ll also likely get the returns you’re hoping for over the long term – minus the high costs you might find elsewhere. Not only that but you can now get the fully automated free financial planning service.

Sign up for Wealthfront and get $5,000 managed for FREE

| Robo-Advisor | Assets Under Management (AUM) | Annual Fee | Account Minimum | Bonuses | Review |

|---|---|---|---|---|---|

| Betterment | $15 billion | 0.25% of account balance. 0.40-0.50% w/ human advisors | None | Up to one year managed FREE | Review |

| Wealthfront | $12 billion | 0.25% of account balance | $500 | $5k managed FREE (Bible Money Matters readers) | Review |

| M1 Finance | $1 billion | FREE (fees for add-on services) | None | Review | |

| Blooom | $3 billion | $10/month any account size | None | FREE 401(k) Checkup | Review |

| Axos Invest | $153 million | 0.24% of account balance. | $500 | Review | |

| Acorns | $1 billion | $1/month under $5k. 0.25% of account balance above $5k. Free for college students. | None | Review | |

| Public | FREE | None | Free stock up to $15 | Review | |

| Stash Invest | $600 million | $1/month under $5k. 0.25% of account balance above $5k. | $5 | $5 New Account Bonus (Bible Money Matters readers) | Review |

| SigFig | $120 million | Under $10k FREE; 0.25% of account balance above $10k | $2,000 | ||

| Personal Capital | $8.5 billion | 0.49% to 0.89% of account balance | $25,000 | Review | |

| Wealthsimple | $5 billion | $0-$99,999 0.50%/yr; $100k+ 0.40%/yr | None | Up to $10k managed free (Bible Money Matters readers) | Review |

| Charles Schwab | $15.9 billion | FREE (They require you to hold 6-30% of portfolio in cash) | $5,000 | ||

| Fidelity Go | N/A | 0.35% of account balance; | $5,000 | ||

| Vanguard | $101 billion | 0.30% of account balance | $50,000 |

Hi Peter,

Would you recommend Wealthfront over Betterment? I have a Betterment account, so I was just wondering how the two compare? Also, I have lost some money since I started investing in a roth IRA at Betterment. Is it more common to lose money during the first year of investing? Do you expect that I will gain more interest over time? I joined Betterment because you said that it has a good proven track record over time. I guess I just need to be patient and wait to start earning interest? thanks, Fred

I think Wealthfront and Betterment are both great, they’re very similar services. They have some small differences in what they invest in, and what their fee structures are. For example, with Wealthfront you can have an account with a minimum of $500 and pay no fees up until $10,000 balance – or $15,000 balance if you use our link. Over $10-15,000 it will be a flat .25% annual fee. With Betterment they have no minimum balance, but have an annual fee of .35% for the first $10,000. Over $10,000 it goes down to .25% annual fee, and .15% over $100,000. So depending on your retirement account balance either one could be the best bet.

With Wealthfront or Betterment they’ll both see ups and downs depending on where the market goes. So this past week or so most of us have seen some downsides to the market. They’re best viewed as long term investing strategies, however, and I think over the long term you’ll be happier with the results.