The Ultimate Guide To Robo-Advisors And Automated Investing Services

By Kevin MercadanteLeave a Comment - The content of this website often contains affiliate links and I may be compensated if you buy through those links (at no cost to you!). Learn more about how we make money. Last edited .

If you haven’t used a robo-advisor yet, or if you’re considering taking the plunge, we hope this ultimate guide to robo-advisors will help you make a well informed decision.

Robo-advisors are rapidly sweeping across the investment landscape, due to their combination of professional management, low fees, and very low minimum account balance requirements.

They work very well for new and small investors, who are looking for a low-cost way to diversify across different asset classes and thousands of securities. But they can even work for the more experienced investor, who may lack the time or motivation that investing requires.

And for the person who’s somewhere in the middle, using a robo-advisor can be a way to break into self-directed investing, while having at least part of your portfolio professionally managed.

So what is a robo-advisor? How do robo-advisors work? What are the benefits and risks? What are the best robo-advisors in the automated investing sphere? What happens when you roboinvest?

Let’s take a look.

Quick Navigation

Guide To Robo-Advisors: What Is A Robo-Advisor?

A robo-advisor is an online, automated investment platform. You sign up for the service, and the robo-advisors handles all the investment details and management for you.

This includes:

Creating your portfolio

Choosing the asset classes and funds that will be included in your portfolio

Maintaining target portfolio allocations through periodic rebalancing

Reinvesting dividends

And often using certain tax strategies to minimize the tax liability from your investments

Once you open a robo-advisor account, your only responsibility is to fund it. The robo-advisor handles everything else for you.

How Do Robo-Advisors Work?

You’ll typically start by completing a questionnaire that will determine your risk tolerance (see below).

Once that’s established, a portfolio diversified between stocks and bonds, and often other assets, like real estate and natural resources, will be created for you.

Robo-advisor portfolios are designed using an investment strategy called modern portfolio theory (MPT). It emphasizes proper asset allocation over individual security selection. This method both enhances returns, while lowering risks.

That portfolio will typically consist of between six and 12 different asset classes, each of which will be represented by a single exchange traded fund (ETF). The advantage of these funds is that they’re very low cost, and since they’re based on popular market indexes, they represent an entire market. With just a handful of ETFs in your account, you’ll own pieces of thousands of different investment securities.

Robo-advisors are particularly well-suited to new and small investors. Once again, they usually have very low minimum opening balance requirements, and some have no requirement at all. Fees are low, and you don’t need to have any investment knowledge at all.

The Risk Tolerance Determination Process

Nearly every robo-advisor starts the investment process by determining your risk tolerance. Basically, that’s your attitude toward potential losses in your portfolio.

Robo-advisors typically make this determination by having you complete a questionnaire of somewhere between six and 10 questions. The more basic questions will ask you what your investment goals are. This may include retirement, saving for college educations for your children, or short-term purposes. They’ll also ask about your time horizon. Do you plan to invest for 10 years, 20 years, or 30 years?

Your stated goals and time horizon will affect how conservative or aggressive your portfolio will be.

But they’ll ultimately get down to a series of questions designed to assess your risk tolerance. Mostly, these are questions to determine how you might feel if your portfolio were to lose value.

They may ask you a question that looks something like this:

If your portfolio were to decline in value by 20%, would you:

Reduce or sell your positions

Hold firm

Buy more investments

If you choose the first answer, your risk tolerance will be considered conservative. The second answer indicates a more moderate attitude toward risk. But the third confirms an aggressive stance. Based on your answers to the questionnaire, your risk tolerance will be assigned one of five different portfolio models, that will generally offer the following options:

Conservative – the allocation might be 60% bonds, and 40% stocks.

Moderately conservative – the allocation might flip to 60% stocks, and 40% bonds.

Moderate – this allocation may have something like a 70/30 stock/bond split.

Moderately aggressive – this portfolio will be primarily in stocks, as much is 80%, with the balance in bonds.

Aggressive – your portfolio will be 90% or more invested in stocks.

The Different Types Of Robo-Advisors

There are three primary types of robo-advisors:

Standalone robo-advisor. These are robo-advisors that aren’t part of a larger investment firm. Examples include Wealthfront and Betterment, the two largest independent robo-advisors in the industry. (We’ll discuss both in detail toward the end of this guide.) They tend to be the most innovative robo-advisors, and often charge the lowest management fees. They’re best for investors who prefer a pure robo-advisor, and aren’t looking for other investment options.

Though these robo-advisors aren’t usually as cutting edge as the independents, they have the advantage that you have the option to have some of your portfolio professionally managed, while also engaging in self-directed investing.

Micro-savings robo-advisors. These are robo-advisors that include an app that enables you to save the money you want to invest. Usually it’s done either through very small contributions, like $5 at a time, or with small “spare change” contributions from your regular spending activity. Examples include Acorns and Stash Invest, both of which will be covered in some detail in our list of robo-advisors in this guide.

Micro-savings robo-advisors are best used by those who have been having difficulty accumulating the funds to begin investing. These apps will help you to both save money, and invest it.

Robo-Advisor Terms To Be Familiar With

Like most investment methods, robo-advisors have their own vocabulary. Some are common to investing in general, but have a special meaning with robo-advisors.

Examples include:

Exchange traded funds (ETFs)

An ETF is a fund of securities designed to match an underlying index. Perhaps the most popular are funds tied to the S&P 500 index, which represents the 500 largest publicly traded companies in the US. Other ETFs may be based on indexes tied to either broader or narrower stock groups, as well as foreign country stocks, or specific industry groups, like healthcare or energy.

Because they’re tied to an underlying index, ETFs are considered passive investments. Since the composition of the index and therefore the ETF only changes when the index changes, stock trades are rare. This keeps investment fees very low, which is one of the major reasons why ETFs are routinely used with robo-advisors.

Passive vs. active investment management

Active investment management involves frequent buying and selling of securities in an attempt by the fund manager to outperform the market. This is typical of mutual funds, which charge higher fees than ETFs.

As described above, ETFs represent passive investments. The fund manager will maintain a portfolio allocation consistent with the underlying index. There will be very little trading in the account, if any at all, which means the fund can only match the performance of the underlying market, but not outperform it.

Portfolio rebalancing

Each portfolio has multiple asset classes. While some classes may rise in value, others will fall. Positions in rising asset classes will be reduced, and the funds moved to those that have declined. This will maintain target asset allocations, as well as enable the robo-advisor to buy asset classes that are low, and sell those that are high.

Rebalancing usually occurs either periodically, or any time there’s a significant change in one or more asset classes in your portfolio. This service is typical of robo-advisors, and does not require an additional fee.

Tax-loss harvesting

This is a common strategy with robo-advisors in which losing investment positions are sold to generate losses to offset capital gains. The sold positions are repurchased at a later date to maintain the desired asset allocation in the portfolio. For example, an S&P 500 index fund from Vanguard might be sold, and later replaced with an S&P 500 index fund from Schwab or iShares. The losses generated by the harvesting enables the continued deferral of taxes on asset sales that produce gains. It’s used only on taxable accounts.

If you’d like to learn more about tax-loss harvesting, check out the Wealthfront Tax-Loss Harvesting White Paper. It’s one of the most comprehensive discussions on the subject available.

Other terms to be aware of

Asset class. This refers to a specific group of similar assets. For example, it can include US stocks, foreign developed stocks, foreign emerging stocks, US bonds, foreign bonds, real estate, natural resources, or other investment classes.

Asset allocation. This is the specific mix of asset classes within a portfolio. For example, your portfolio may be 70% invested in stocks, including both US and foreign stocks. The remaining 30% may be invested in bonds, including high-grade US corporate bonds, international bonds, and US Treasury securities.

Advisory fee. This is the fee charged by investment managers, including robo-advisors, to manage your portfolio. Robo-advisor fees generally range between 0.25% and 0.50% of your average account balance. This is well below the 1% to 2% typically charged by traditional human investment advisors.

Automatic dividend revinvesting. Most robo-advisors automatically reinvest dividends generated by the investments held in your portfolio. This will not only enable your portfolio to grow faster, but it can also assist with rebalancing.

Socially responsible investing (SRI).SRI is an investment strategy in which securities are chosen based on social justice, environmental sustainability and alternative energy/clean technology efforts. The strategy will avoid investing in companies not considered to maintain practices consistent with these standards. It represents an opportunity for investors to invest in what they believe in. SRI is now commonly offered by many robo-advisors.

Smart Beta.Smart Beta is a more aggressive investing strategy, that involves improving returns and diversification, and reduced risk by investing in customized indexes or ETFs. For example, the investment manager may generally invest in a common index, but give heavier weight to certain stocks or sectors considered likely to outperform the market.

The Benefits Of Investing With Robo-Advisors

You don’t need to know anything about investing. Even if you know nothing about stocks and bonds or portfolio allocations, you can invest with a robo-advisor. They handle all the details for you, and all you need to do is fund your account.

Professional investment management. This means you can invest your money, then get on with the rest of your life. Robo-advisors are staffed with people who invest money for a living, which will free you up to virtually ignore the investment process, knowing your money is in safe hands.

Low fees. The typical fee range for robo-advisors is between 0.25% and 0.50%. That means you can have a $10,000 account managed for just $25 or $50 per year. Some robo-advisors even charge no fee at all. Meanwhile, there’s no commissions on individual trades within the account. You pay one fee, and that covers all your expenses. It’s one of the most cost-effective ways to invest ever designed.

Diversified portfolio with a very small investment. Because of the use of asset allocations through ETFs, an account with just a few hundred dollars can be spread across thousands of individual securities. That will give you a level of diversification you can’t create with the same amount of money through self-directed investing.

Many are tax efficient. Income taxes are minimized when income generating assets, like bonds, are held in tax-sheltered accounts, like IRAs. Capital gains generating assets are held in taxable accounts, where they get the benefit of lower long-term capital gains tax rates. And we’ve already discussed tax-loss harvesting as a strategy to further lower and defer capital gains taxes.

Can be customized to fit your investor profile. Since each portfolio will be based on your own risk tolerance, the asset allocation will be unique to you.

The Risks Of Robo-Advisors

You’re not likely to outperform the financial markets. As passive investments, robo-advisors only match the underlying markets. You’re highly unlikely to see your portfolio perform any better than the general markets.

You generally can’t make your own investment selections. Robo-advisors are fully automated, with specific investments chosen from a short list of options by the platform. You won’t be able to add investments of your own choice to the mix. Though some robo-advisors are beginning to give investors at least limited choice over their investments.

No financial advice. To keep management fees low, robo-advisors limit customer contact. While you may be able to speak to a representative about technical service matters, they won’t provide specific investment advice. But once again, some robo-advisors are now experimenting with providing at least limited financial advice. This is very much an industry that’s in a state of flux.

Fees are higher than ETFs. Though robo-advisor fees are much lower than other types of investment management options, they’re not absolutely the least expensive way to invest. For example, if you work to create a portfolio of ETFs based on models offered by robo-advisors, you could avoid the management fee entirely. ETFs don’t have annual fees, and can usually be bought and sold through investment brokerages for just a few dollars per trade.

Of course, you then have to handle all the investment management yourself.

You won’t be protected from market declines. One of the caveats of robo-advisors is that they’ve mostly come about since the last bear market ended in 2009. This may have caused investors to believe they can’t lose money on these platforms. But since the investments held in each portfolio are designed to match the performance of the underlying market, you can lose money if the markets decline.

The Top Robo-Advisors

Though the whole robo-advisor phenomenon is barely a decade old, there are already dozens of participants in the automated investing service space. We aren’t going to look at all of them today, but we will review some of the top contenders for the best robo-advisor prize.

Comparison Of Betterment vs. Wealthfront vs. Wealthsimple vs. Empower vs. M1 Finance vs. blooom vs. Axos Invest vs. Acorns vs. Stash Invest

Below are summary reviews of nine of the best robo-advisors that have been fully reviewed here on Bible Money Matters. You can click through to the full review on each, but the summary below provides a side-by-side comparison to help you choose the best one for you. They’re listed in no specific order.

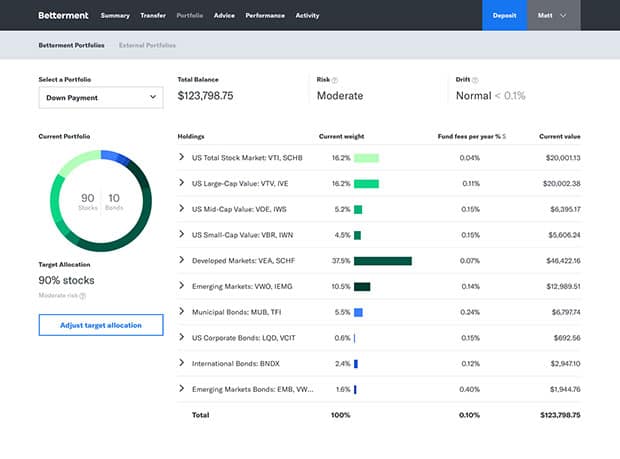

Betterment

Betterment is the original robo-advisor, and the largest standalone platform in the industry. It’s also one of the major innovators in the field, being one of the first to introduce tax-loss harvesting, Smart Beta, and other robo-advisor specializations.

Betterment is now introducing live financial advisors to the mix. You can even purchase financial advice packages for specific life events, like retirement planning and college planning. You can open a basic account with no money at all, and a very low annual fee of 0.25%.

Betterment features:

Minimum investment: $0 Digital; $100,000 Premium

Annual advisory fee: Digital: 0.25% to $2 million, then 0.15%; Premium 0.40% to $2 million, then 0.30%

Accounts available: Individual and joint taxable accounts, IRAs and trusts

Asset classes in your portfolio: US and international stocks and bonds

Tax-loss harvesting: Yes, on all taxable account balances

Smart Beta: Yes

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Customizable asset allocations (on accounts of $100k+); fixed income portfolio

Better Business Bureau rating (on a scale of A+ to F): A+

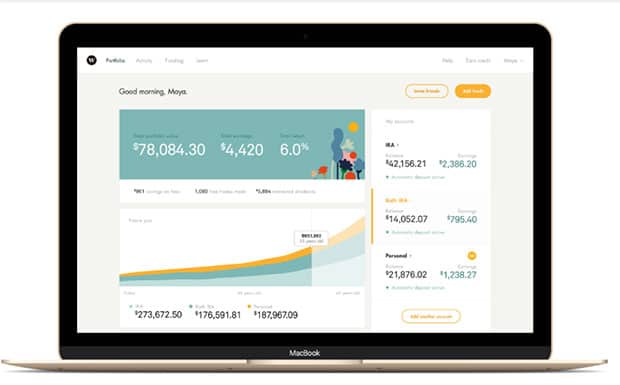

Wealthfront is the second largest independent robo-advisor, and Betterment’s primary competitor. They specialize in tax-loss harvesting, offering stock level tax-loss harvesting for taxable accounts with $100,000 or more.

Their portfolios are also more diversified, adding real estate and natural resources to the basic portfolio mix of stocks and bonds. They also offer a portfolio line of credit, enabling you to access up to 30% of the value of your account, with repayments on your own terms.

Wealthfront features:

Minimum investment: $500

Annual advisory fee: 0.25%

Accounts available: Individual and joint taxable accounts, IRAs, trusts and 529 college savings plans

Asset classes in your portfolio: US and international stocks and bonds, real estate and natural resources

Tax-loss harvesting: Yes, including stock level tax-loss harvesting on accounts over $100,000, increasing the opportunity to generate tax losses

Smart Beta: Yes

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Ability to add individual stocks to your portfolio on larger account balances

Better Business Bureau rating (on a scale of A+ to F): F (based on failure to respond to two complaints out of three)

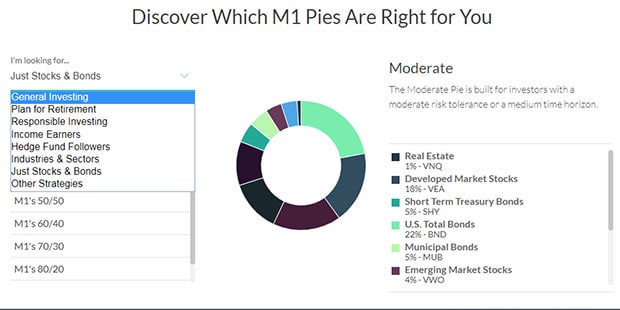

M1 Finance is one of the most unique of all robo-advisors. Rather than creating a portfolio for you, the platform enables you to create what they referred to as “pies”. Each pie is comprised of slices of ETFs and individual stocks.

You can hold as many as 100 securities in each pie, and create as many as you like. M1 offers more than 60 pie templates, but you can create your own. Once you build a pie, it will be fully managed for you by M1 Finance. In this way, you have the unique combination of being able to create your own portfolio, but having it fully managed for you.

M1 Finance features:

Minimum investment: None

Annual advisory fee: None

Accounts available: Individual and joint taxable accounts, IRAs and trusts

Asset classes in your portfolio: Your choice

Tax-loss harvesting: No

Smart Beta: No

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Create your own portfolios from stocks and ETFs

Better Business Bureau rating (on a scale of A+ to F): Not rated

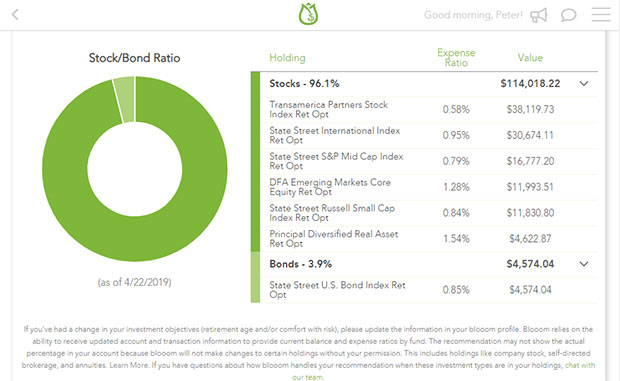

blooom is another unique robo-advisor service. It’s virtually the only investment management service available for employer-sponsored retirement plans. It doesn’t require participation by your employer either.

When you subscribe to the service, blooom takes over the investment management, including investment selection and rebalancing.

The service works with the investment offerings available in your plan. It will generally favor lower cost funds in creating your asset allocation. It will even perform a free retirement plan analysis, with recommendations of both a specific asset allocation and use of certain funds. It’s the robo-advisor for your 401(k).

Axos Invest (formerly known as WiseBanyan) is a free robo-advisor service that requires no minimum initial investment. However, they do charge an extra fee on taxable accounts that include tax-loss harvesting.

Because of the absence of a minimum investment or fees, Axos Invest is an excellent choice for new and small investors.

Axos Invest features:

Minimum investment: $0

Annual advisory fee: None

Accounts available: Individual and joint taxable accounts, IRAs

Asset classes in your portfolio: US and international stocks and bonds, real estate

Tax-loss harvesting: Yes, but at the lesser of $20 or 0.02% per month

Smart Beta: No

Socially Responsible Investing: No

Mobile app: Android and iOS

Unique features: Free service with no minimum initial investment

Better Business Bureau rating (on a scale of A+ to F): F (based on length of time business has been operating)

Acorns is actually part robo-advisor, and part micro-savings app. It’s perfect for the newbie who not only wants to begin investing, but needs to accumulate the funds to do it. Acorns enables this through a process called spending “Round Ups”. You link spending accounts to the app, and they round up your payments. For example, a charge of $4.25 is rounded up to $5, with $0.75 allocated for investing. Once you have at least $5 will in roundups, the money will be transferred over to the Acorns robo-advisor.

If you want to accelerate the savings and investment process, you can also make scheduled deposits or even lump sum deposits. Once in the investment account, you can sign up for one of five different portfolios – conservative, moderately conservative, moderate, moderately aggressive, and aggressive.

Acorns features:

Minimum investment: $0, but $5 to begin investing

Annual advisory fee: $1 per month up to $1 million, then 0.25% on higher balances; free for college students under 24, but higher for IRA accounts

Accounts available: Taxable accounts and IRAs

Asset classes in your portfolio: US and international stocks and bonds, real estate

Tax-loss harvesting: No

Smart Beta: No

Socially Responsible Investing: No

Mobile app: Android and iOS

Unique features: Micro-savings app enabling you to save money for investing by rounding up your purchases, and transferring the money to your investment account; free for college students

Better Business Bureau rating (on a scale of A+ to F): F (47 complaints filed)

Stash Invest is more of a micro-savings and investment app, than an actual robo-advisor. They allow you to invest in increments of just $5, and enable you to invest in both ETFs and individual stocks. Investment portfolios are prebuilt templates, offered based on your risk tolerance level.

One of the areas where Stash Invest departs from more traditional robo-advisors is that they don’t actually manage your portfolio for you. Instead, they recommend a portfolio, and necessary adjustments going forward. In effect, you’ll be managing your own portfolio, based on their investment advice.

Stash invest:

Minimum investment: $5

Annual advisory fee: $1 per month to $5,000, then 0.25%

Accounts available: Taxable accounts, IRAs and custodial accounts

Asset classes in your portfolio: More than 40 prebuilt investments, comprised of both ETFs in individual stocks

Tax-loss harvesting: No

Smart Beta: No

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Micro-savings app + robo-advisor recommendations, but not direct management

Better Business Bureau rating (on a scale of A+ to F): A

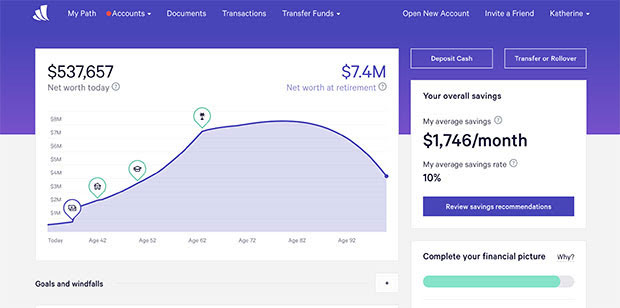

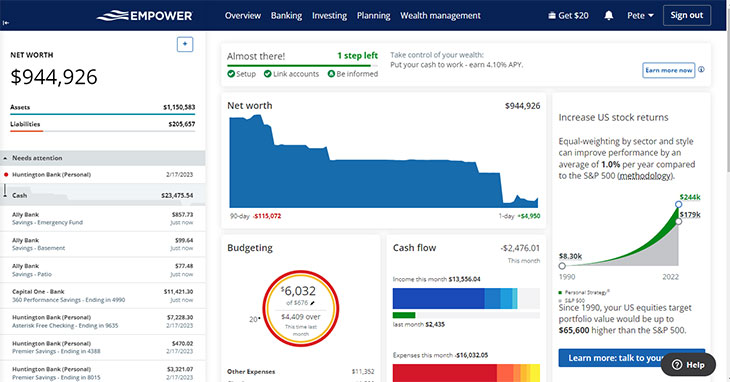

Empower Personal Dashboard is actually a wealth management service, that uses robo-advisor investment management techniques. That makes them more like a traditional human-guided investment advisory service but at much lower fees.

Empower provides its financial software, which is completely free to use. It acts as a financial account aggregator and provides limited budgeting capabilities. But it can also do a portfolio analysis, offering recommended changes to your asset allocations.

The Wealth Management service is the premium investment service, and provides full investment management as well as financial advisory services. In this way, Empower goes well beyond the typical robo-advisor.

Empower features:

Minimum investment: $0 for the free financial software; $100,000 for the Wealth Management service

Annual advisory fee: 0.89% up to the first $1 million, then on a sliding scale down to 0.49% at $10 million or more

Accounts available: Individual and joint taxable accounts, IRAs, 529 college savings plans; recommendations, but not management on 401(k) plans

Asset classes in your portfolio: US and international stocks and bonds, and alternatives, including real estate and commodities (gold and energy)

Tax-loss harvesting: Yes

Smart Beta: Yes

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Free financial software, complete with portfolio recommendations; complete wealth management for accounts of $100,000 or greater

Better Business Bureau rating (on a scale of A+ to F): F (length of time the business has been operating)

Wealthsimple specializes in socially responsible investing as well as Halal investing (see description below). Their fee structure is higher than that of other robo-advisors, but the service is available free to residents of Canada.

The Wealthsimple Black program is the premium service, requiring a minimum investment of $100,000. But it offers financial planning with a Wealthsimple advisor, as well as tax-loss harvesting and VIP Priority Pass access to more than 1,000 airline lounges in over 400 cities around the world.

Wealthsimple features:

Minimum investment: $0

Annual advisory fee: 0.50% to $100,000; 0.40% on higher balances

Accounts available: Individual and joint taxable accounts, IRAs and trusts

Asset classes in your portfolio: US and international stocks and bonds

Tax-loss harvesting: Yes

Smart Beta: No

Socially Responsible Investing: Yes

Mobile app: Android and iOS

Unique features: Offers Halal portfolio, comprised of investments deemed to be acceptable under Sharia law; this portfolio is comprised entirely of stocks, since interest on debt investments is considered prohibited

Better Business Bureau rating (on a scale of A+ to F): A

The answer to this question really depends on your own investment knowledge. If you have a long, successful history of investing your own money, you’ll probably be less interested in robo-advisors. But if you have little or no investment experience, robo-advisors are a go-to investment choice.

As a new or small investor, it can make sense to put 100% of your investments into a robo-advisor. The only caveat is to make sure that you have an adequately stocked emergency fund to cover more immediate financial needs. This should be an amount sufficient to cover between three and six month’s living expenses. The emergency fund will eliminate the need to liquidate your investment account for an unexpected expense or a temporary loss of income.

But even if you’re an experienced investor, you might still consider using a robo-advisor. If you don’t have time or the inclination to manage your own portfolio, robo-advisors are a low-cost way to do it.

And if you’re somewhere between inexperienced and very experienced, you may want to consider splitting your portfolio between a self-directed portion and a managed portion with a robo-advisor. If you find your results are better with the robo-advisor, you may want to increase your investment. But if you’re finding success with self-directed investing, you can gradually begin moving funds away from your robo-advisor.

With the combination of professional management, low initial investments, and very low fees, robo-advisors are fast becoming an investment tool that can benefit most investors.

If you’ve always wanted to add commercial real estate to your investment portfolio, but don't have the capital, take a look at real estate crowdfunding.

Betterment offers the best combination of investment options, tax-loss harvesting and low fees of any robo-advisor - with no minimum investment requirement.

Wealthsimple has become one of the premier options for people looking to have a simple, effective and automated investment portfolio. Here's our review.

Last Edited: 20th February 2023 The content of biblemoneymatters.com is for general information purposes only and does not constitute professional advice. Visitors to biblemoneymatters.com should not act upon the content or information without first seeking appropriate professional advice. In accordance with the latest FTC guidelines, we declare that we have a financial relationship with every company mentioned on this site.

About Kevin Mercadante

Kevin Mercadante is a follower of Jesus Christ, a husband, father, and freelance professional personal finance blogger for hire, and the owner of his own personal finance blog, OutOfYourRut.com. He has backgrounds in both accounting and the mortgage industry.

{kind=link}

Share Your Thoughts: