About 6 months ago I discovered two cool new services that had recently launched, both of which were a part of the recent trend towards automated saving and investment account options.

The first one was an free online savings account from Digit, an account that helps take the busy work out of saving. It analyzes your checking account daily and at regular intervals it saves small amounts of money from your checking and puts it into your Digit savings account – without your intervention. It allows you to save money, a little bit at a time, without even realizing it.

The second account is a free automated investment adviser from the folks at Axos Invest. When you have an investment account from Axos Invest, their system will allow you to regularly invest in a taxable or tax-advantaged retirement account, and it will automatically invest your funds in a portfolio of low-cost ETF index funds. It’s a great new long term investing site, along the lines of Betterment or Wealthfront, but without any account management costs.

Digit and Axos Invest are both big on the idea of automating things in order to make them more efficient, more cost-effective and better for your bottom line. I liked the idea behind both sites, and after signing up I decided to take them on a trial run and to run an experiment.

Just how much could I save automatically for the year using Digit’s tools? How much would I be able to invest at no cost using Axos Invest? How much intervention would I need to have – and just how much could I save over time? First, let’s take a brief look at these two accounts.

Quick Navigation

Digit Savings Account

According to Ethan Bloch, the founder of Digit, the company was started to help people, “maximize their money, while at the same time driving the amount of time and effort it takes to do so as close to 0 minutes per year as possible”

So how does Digit work? You sign up for an account, and link your checking account. Digit will then analyze your income and expenses, find patterns and then find small amounts that it can set aside for you – without any pain for you.

So once you sign up and turn on auto-savings, every 2 or 3 days Digit will transfer some money from your checking to your savings, usually somewhere between $5-$50. Digit won’t overdraft your account, and they have a “no overdraft guarantee that states they’ll pay any overdraft fees if they accidentally overdraft your account.

Open Your Digit Savings Account

Axos Invest Investing Account

Axos Invest launched with the goal of being the world’s first completely free financial advisor. Their founders had a mission “to ensure everyone can achieve their financial goals, which starts with investing as early as possible. This is why there is no minimum to start and we do not charge fees.”

Axos Invest’s founders understood that one of the drags on the typical person’s portfolios is the fees that they’re paying to invest, as well as the friction point of having to invest thousands of dollars to start. They changed that with no minimums to invest, and no fees charged for investing. Axos Invest will be releasing some premium add-on products for their users, which they will charge for, but a basic investing account will not cost anything beyond the mutual fund expense ratios associated with your investments.

What do you invest in with Axos Invest? Axos Invest will invest your funds based on Modern Portfolio Theory (MPT). Your investments will be diversified, low cost and recognize the value of long term passive investing by investing in ETF index funds.

Open Your Axos Invest Investing Account

The Digit + Axos Invest Experiment (D+AI Experiment)

So for my Digit and Axos Invest experiment, the goal was not only to try out these two free products, but also to show just how easy (and low cost) it can be to invest.

When I started in early February my goal was to allow Digit to automatically save money from my checking account and put it into my Digit savings. Whenever the amount in my Digit savings reached $75 I would transfer that money over to my Axos Invest account and invest it in their highly diversified set of ETF index funds.

Why was I doing it this way? I did it this way because Axos Invest has no minimums and you can buy fractional shares, so why not? I can transfer money in small chunks, and engage in a bit of dollar-cost averaging while I’m at it.

So how are things going now that we’re more than half the way through the year?

The Experiment In Progress

Once I had setup my Digit and Axos Invest accounts I put the plan in action and allowed my Digit account to start saving on my behalf. After a few days Digit had started saving small amounts in my account. There was $7.50 here, $15 there – as well as $5 deposits for referrals of friends and readers. Multiple transfers and deposits ended up adding up to larger amounts over a couple weeks time. The first time that I invested with Axos Invest I deposited $186 that had accrued in my Digit account.

From then on every time the amount reached around $75 or more, I would transfer the money to Axos Invest.

Amounts Withdrawn And Invested So Far

I’m now just over 5 1/2 months into my little experiment, and so far I’ve withdrawn my Digit savings balance and invested it in my Axos Invest Roth IRA 14 times. The amounts were:

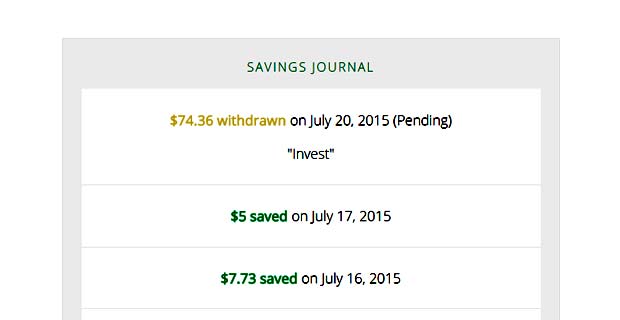

- $74.36

- $79.76

- $121.75

- $82.03

- $95.67

- $81.27

- $93.28

- $109.47

- $76.20

- $99.08

- $99.32

- $90.88

- $74.72

- $186.00

Here’s a screenshot from my Digit account showing my latest withdrawal for the purpose of investing.

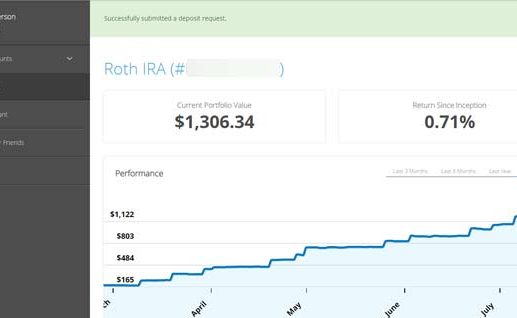

After withdrawing the money I then transfer it from my checking account over to Axos Invest. Here’s a screenshot of one of my latest deposits with Axos Invest. In the screenshot you can also see how deposits are then used to purchase fractional shares of the ETF index funds used in the account.

Once my latest deposit of $74.36 goes through I’ll have $1380.70 invested at Axos Invest.

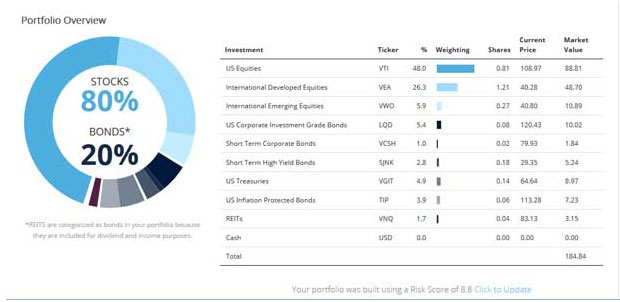

Here’s my portfolio’s asset allocation in my Axos Invest account. It is a bit more aggressive than in my other retirement accounts.

The funds that Axos Invest currently uses, and their expenses, are shown below (and are subject to change)

- Vanguard Total Stock Market ETF (VTI): 0.05%

- Vanguard FTSE Developed Markets ETF (VEA): 0.09%

- Vanguard FTSE Emerging Markets ETF (VWO): 0.15%

- Vanguard Intmdte Tm Govt Bd ETF (VGIT): 0.12%

- Vanguard Short-Term Government Bond Index ETF (VGSH): 0.12%

- State Street Global Advisors Barclays Short Term High Yield Bond Index ETF (SJNK): 0.40%

We’ll see what kind of returns my account sees over the coming months/years, but I’m sure it will about match what the market does. Since I’m not paying any account management fees as well, I’ll be coming out ahead as compared to some other robo-adviser competitors.

How’s It Going So Far?

So how is the experiment going so far? I think it’s been pretty successful. I’ve saved $1380.70 over the 5 1/2 month period. If we round that up to 6 months it means an average saved of about $230.12/month.

Multiply the $230.12 by 12 months and it means that if I continue this experiment for an entire year, I could expect to see somewhere in the neighborhood of $2761.40 saved for the year.

While $2761.40 isn’t going to profoundly change someone’s life, it isn’t a small amount of money either.

If you look at that $2761.40 amount, it’s just over half of the annual $5500 contribution limit for a Roth IRA. So essentially, over half of my year’s worth of Roth IRA contributions are happening without any pain for me.

The money is coming out in small chunks, so small I don’t even notice. Over time those small chunks are adding up to larger dollar amounts that do make a difference to my long term strategy. All in all I think it’s a pretty powerful idea, making savings and investment happen automatically in the background, with only a small amount of intervention needed from you. The fact that both of these tools are also free is just icing on the cake.

Join In The Digit & Axos Invest Experiment

Interested in joining the “Digit and Axos Invest Experiment”? I invite you to join in! The only risk you’ll have by joining is that your retirement accounts will grow over time and that you’ll likely be paying fewer costs than your current retirement account provider.

Open accounts with both services, set Digit to save automatically, and get started. You’ll be glad you did. Let’s see how much you can invest – with minimal effort or intervention!

The hardest part of saving is budgeting and then contributing to your account. But making it seamless (and painless) Digit does an incredible job at handling the daunting task. We’d like to know if you also have a savings account you contribute to regularly, in addition to Digit? If so, what are your strategies around that?

Yes, I have other savings accounts beyond Digit. We have one all encompassing emergency fund savings account that will hold 8-12 months of expeneses when we’re finished. We then also have several separate savings accounts for big savings goals. We have a “next car” savings accounts that has automated debits every month, “next vacation” fund that debits every month, and a couple of others that serve as dumping places for funds for other regular expenses that we need to save up for throughout the year. Essentially we save to plan ahead for all those foreseen and unforseen expenses throughout the year.