Every year, the credit reporting agency Experian puts out a report on credit trends in the United States. The Fourth Annual State of Credit takes a look at trends divided by geography and age, as well as other demographics.

I always find it fascinating to have a look at how I stack up as compared to my peers.

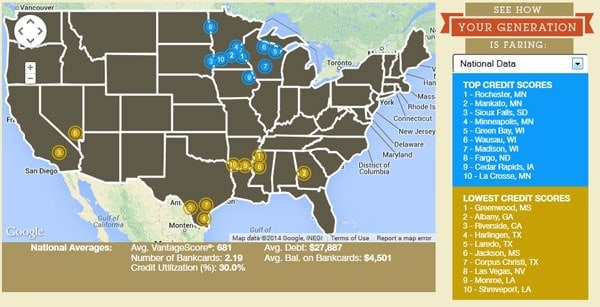

Geographic Trends

First of all, I looked at the report’s map showing the cities with the best and worst credit scores. I found it interesting that almost all of the best credit scores are located in the upper midwest. Minnesota and Wisconsin had most of the cities with the top credit scores, with a some sprinkled in North Dakota, South Dakota, and Iowa.

The 10 cities with the worst scores are all below the Mason-Dixon line, with most of them located in the Southeast, with Riverside, CA and Las Vegas, NV as the two in the Southwest.

None of the cities with the worst or best credit scores are located in Utah, my home state.

Generational Data

The Experian report divides the generational data into four categories: Greatest Generation (66 +), Baby Boomer (47 – 65), Generation X (30 – 46), and Millennial (19 – 29). I’m firmly in Generation X for the purposes of this report.

According to the report, the Millennials need the most help figuring out how to build their credit. This isn’t exactly surprising. After all, few schools teach financial literacy, and lessons many kids get about credit from their parents often consist of this advice: “Don’t get credit!”

This doesn’t prepare young adults to head out into the world and begin building their credit in meaningful ways. Instead of trying to scare kids about credit, I think it makes more sense to teach them about responsible credit use in combination with solid financial skills.

You have a great chance when you’re in your early 20s to create a solid credit profile, and learning how to do that effectively can mean a better financial result down the road.

National Averages

No report of this nature would be complete without national averages. According to the Experian report, the average debt in the United States is $27,887. The good news is that debt isn’t mostly credit cards. Indeed, the average balance on bank cards is $4,501. I remember a few years ago when the average was higher than that, so it’s clear that progress has been made in terms of the average person paying down debt.

The average number of bank cards that consumers have in the United States is 2.19. This is one area in which I am above average. My husband and I have six credit cards between us. This probably isn’t the most efficient use of our credit, though. I need to re-evaluate the cards and their rewards programs and make sure that I’m sticking with some sort of plan. I tend to get lazy and drift off the program if I’m not careful. We pay off what we spend, but I don’t always use the card to give maximum results if I’m not paying attention.

Take a look at the data, and figure out how you stack up. Are you average for your location and generation? Where do you fit with the national average? Answering these questions can help you figure out whether or not you need to make changes.

Related:

It’s nice to see my home state of Minnesota is well represented in the top credit scores. I’m not sure why the top credit scores have seemed to center on the upper midwest like that, Very interesting.

I think our household is above average for our area, and for the national average, so we must be doing something right! We only currently have 1 credit card, and a 0% credit utilization with zero consumer debt.Credit scores are well above average as well – which was nice when getting a mortgage for our house this summer!