This week as I was preparing for the weekly Money Mastermind Show, I was thinking a lot about the subject of our show, the idea of living without credit. Would it be possible to live in our society without a credit score and history, or is it so ingrained in our culture that it would be next to impossible to live outside of that paradigm?

In talking with our guest on the show, Steve Stewart of MoneyPlanSOS.com I came to the conclusion that it is in fact possible to live without using credit – or having a credit history, but that in some instances it will make your life a bit harder than if you did engage in using credit to some degree. The system is just setup to use the credit score as a way to gauge a person’s ability to repay, and in some cases getting around that may mean jumping through some extra hoops – and in some cases – cost you some extra money.

Quick Navigation

Credit Reporting Goes Back To The 1860s

In the U.S. there are around 2 billion data points entered every month into credit records, and there are around 1 billion credit cards actively being used.

The idea of determining someone’s creditworthiness goes back a long way. Back in the 1860s local merchants would put together lists of individuals who they deemed poor credit risks, that they would then share with other local merchants. These lists were essentially the first credit reporting tools.

As populations became more mobile and moved around the country more freely, larger regional and national credit bureaus as we know them began to crop up. They’ve continued to grow to the point where today we mainly use credit scores and reporting from the big three credit reporting agencies of Transunion, Equifax and Experian.

Here’s the Money Mastermind Show as we discuss living without credit:

Credit Is Used In So Many Places

In today’s world you can have your credit checked in just about any situation where you might be asking for a line of credit, signing up for a payment plan or even at times if you’re trying to get a job.

Things That Will Sometimes Require A Credit Check:

- Mortgages: Lenders will review your credit reports and scores from all three agencies in the application process. To get the best rates you’ll likely need to have a credit score above 700-750.

- Auto loans: Lenders will typically rely on your credit score, and if you have above a 750 credit score you can typically receive the best loan rates.

- Student loans: Private student loans may require a credit check, although federal student loans don’t require a credit check.

- Insurance: Insurance companies will use your credit information along with your application data to help determine your rates and terms. Reports and scores used by the insurance industry are a bit different than the ones used by creditors and lenders, but it will basically be the same data.

- Credit cards: When you apply for a card the bank will review your credit score to see if you qualify for the card you’re applying for. Depending on your score you can also receive a lower or higher APR.

- Cell phone plan: Before you get a service plan mobile providers will often check your credit score, and if you have credit issues you may be asked to put a large down payment, or pay extra for your contract.

- Government assistance or licensing: Government agencies can access limited information from your credit files without permission, and thorough credit checks can be required if you are applying for certain licenses or government assistance.

- Rental: Prospective landlords will often use your credit report to look for a pattern of missed payments or other negative marks on your record. If you do, they may require larger deposits, co-signers, or you could be denied housing.

- Jobs: Some jobs, especially in financial sector, may review your credit report. They must get written permission, and if they plan on taking “adverse action” based on the information in the report, they have to notify you and give you a copy of the report.

- Utilities: Electric, gas, cable TV and other providers may check your credit report with your permission. If you have issues on your report you may have to put down a deposit, get a co-signer, or pay higher rates.

How Can You Live Without Credit – When So Many Require It?

So many places require that they be able to check your credit and show your creditworthiness, so what can you do if you’re not engaged in world of credit – and you don’t have a credit score?

There are ways to work around the requirements for a credit card or credit check.

- Manual underwriting to get a mortgage: While this isn’t as common as it one was, there still are a few places that will give you a loan by manually underwriting your loan. In some cases it may cost a bit more, however, because it is a more work intensive process for the bank.

- Get a pre-paid phone: It’s probably a better deal anyway and requires no credit check since you pre-pay every month for the phone.

- Pre-paid TV service: Some TV services have no credit check, and others will do pre-paid service – like cell phones.

- Rentals: To rent you may have to pay a larger deposit, demonstrate your financial soundness, or show a good rent to income ratio to your landlord. It may also help to get recommendations from past landlords, have a co-signer or to find an independent landlord that doesn’t do a credit check.

- Car rentals: To rent car some places may require that you have a credit card vs. a debit card. Make sure before renting. Also be aware that some may place large holds on funds in your account if debit is used. Ask about this as well and choose where you rent a car wisely.

- Hotels: Sometimes if you don’t have a credit card you may h ave to secure your hotel room with a cash deposit, and not all will. You may have to call a couple.

The point is, there are options if you don’t use credit, you just have to be creative, and in some cases jump through a few extra hoops.

Alternative Credit Scoring For Those Living Debt Free

If you don’t have any credit history at all because you don’t use debt, you may need to get creative and use a service like eCredable.

eCredable will help you to prove your creditworthiness by giving lenders an “All My Payments (AMP)” score, which will take into account things like your utility bill, rent payments, daycare costs and other monthly bills. All things that are never factored into a FICO score. Even though you don’t have a FICO score – which shows how you manage debt – you’ll still be able to prove you’re worthy of getting a loan like a mortgage.

Having Good Credit Is Pretty Simple

If you’re younger and looking to establish good credit, I wouldn’t suggest going out and getting a bunch of credit cards to prove you’re worthy, but if you do have any debts, the easiest way to have good credit is to simply make your payments. Here’s what makes up your credit score:

- Payment History (35%)

- Amounts Owed (30%) Keep it less than 30% of total limit

- Length of Credit History (15%)

- New Credit (10%)

- Types of Credit Used (10%)

The biggest component of your score is your payment history, along with amount owed versus your total limit. For my wife and I both of us have a credit score between 760-800, and we’ve maintained that score simply by paying our bills and never missing payments. Our only real debt right now is the mortgage, and we typically don’t use credit cards, so essentially we’ve got a good score by paying our mortgage and staying current – that’s it. No magic formula.

Checking Your Credit Scores

Staying top of my credit score isn’t something I do all that often, but I will check it every once in a while to see where I’m at. At the end of last year, however, I was checking more often because we were in the midst of getting a new home mortgage.

So where are some places you can check your score? Here’s a few places that I usually go to check because they will give you a free credit score, without using a credit card, based off of your profile from one of the three major credit bureaus. It should be noted that these three scores are not the actual FICO score that the banks are using, but I have found that it is usually pretty darn close to what they show for a number.

I checked them last night in preparation for the show, just to see where I was. Check them out yourself as well, they don’t cost a thing!

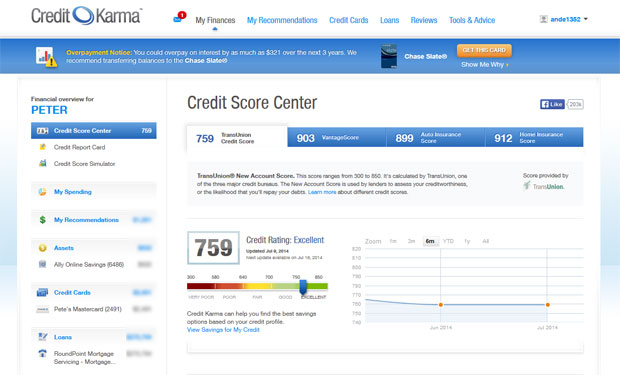

Credit Karma (Transunion)

Credit Karma will help you to manage your finances, and specifically your credit situation. They’ll also give you a free Transunion credit score, updated monthly. My credit score came back at 759 through their site. (Full review here)

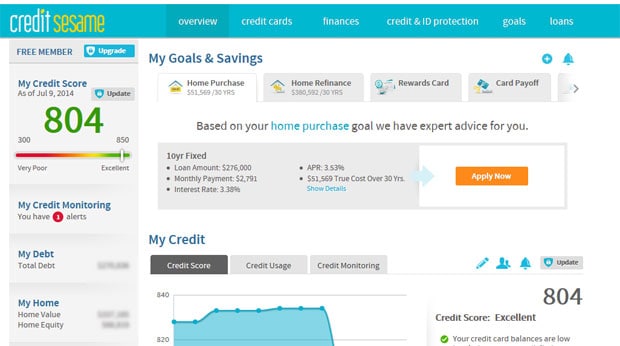

Credit Sesame (Experian)

Credit Sesame is a similar site that aims to give you an overall picture of your credit situation, and help you to find lower cost home loans, credit cards, etc. My credit score through Credit Sesame, which is an Experian score, came back at 804. (Full review here)

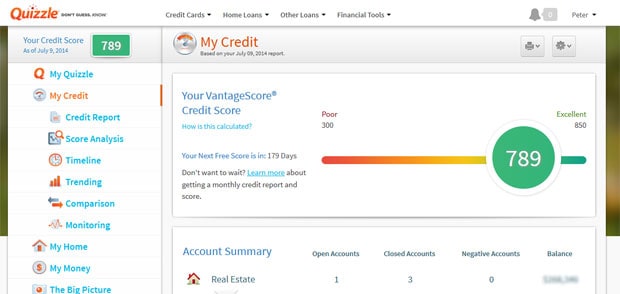

Quizzle (Equifax)

Quizzle gives you a full overview of your financial picture, and will give you a credit score from Equifax as well as a full credit report. My score through Quizzle showed 789. (Full review here)

In addition to checking your scores, don’t forget to check your 3 agency credit reports, once a year at AnnualCreditReport.com

What is a good credit score?

So just what is a good credit score? This table lays it out for you.

| Credit Score | Description |

|---|---|

| 750-850 | Excellent credit. |

| 680-749 | Good credit. |

| 620-679 | Average credit. |

| 560-619 | Poor credit |

| 300-559 | Bad credit. |

For a more in depth discussion of what a good credit score is, check out this article:

Why Try To Live Without Credit?

So why would people even want to attempt to live without credit?

- When spending on a credit card, people tend to spend 12-18% more. The reason? Spending cash hurts more.

- According to the Experian Intelliview tool the average credit card balance per consumer was recently reported to be $3,779, with many having much more. Why live with that kind of debt? It is a weight on your shoulders.

- Credit cards encourage irresponsible spending by promoting a culture that says “things can make you happy”. They are a way to extend people’s income and live above their means. It leads to false sense of security and a lack of planning.

- Lower your risk of identity theft by using less credit. No or fewer credit cards, means less information to steal!

- Credit card spending leads to higher prices due to swipe fees.

- Consumer reports found that people who have rewards cards often end up spending more money than those with a regular card.

- Rewards aren’t what they’re cracked up to be: Consumer Reports released a study where they found that about 85 percent of U.S. households participate in at least one rewards program, but GMAC Mortgage and Harris Interactive found that more than 41 percent of reward cardholders either rarely or never even bother to use their rewards.

- If you carry a balance, the rewards are outweighed by the interest you’re charged.

- Simpler less stress filled existence. No late fees to worry about, no payments. No need to juggle multiple rewards accounts, rotating categories or anything else.

Are There Benefits To Using Credit?

There certainly can be benefits to using credit. Depending on how you use credit can determine whether those benefits are worth it or not.

- Added credit card benefits can be attractive. Anti-fraud protection (although many debit have this too, usually if run as credit), travel insurance, rental car insurance, purchase protection, warranty and more.

- If your accounts are compromised, it isn’t your cash at stake, but the bank’s money.

- Rewards can be lucrative if you do them right. If you play the game correct and don’t overspend, you can get plenty of perks like cash back, free flights, etc. Just don’t carry a balance or have late payments!

- Flexibility of having the card if extra cash is needed.

- Build a solid credit history through responsible use.

- The convenience factor. Using credit cards makes things like travel, booking a hotel room or rental car, easier.

What Are Some Alternatives To Living With Credit?

National Foundation for Credit Counseling found in an online poll that fully 64 percent of Americans would use a source other than their savings account in order to pay for an unplanned $1,000 expense.

If you want to live a debt free lifestyle, it will likely require some extra effort. Here are some things you can do.

- Save a nice 12 month emergency fund: If you’re not using your credit card as your emergency fund, you’ll need some cash to cover those unforeseen costs.

- Set goals for things you want to buy: Setup a budget, and used goal based savings accounts. (Accounts and savings for car purchases, vacation account, etc)

- Use debit cards: Debit cards these days have most of the same protections as credit cards, as long as you use them correctly, and check terms before getting an account.

- Get necessary insurance to cover risks: Make sure you’re covered with insurance to cover the risk of catastrophic expenses. Save an emergency fund to cover the deductibles.

- Go without!: Instead of leveraging yourself in order to buy things you don’t need, take a second look and reconsider your purchases.

- Use alternative products: Get manual underwriting on your mortgage, instead of relying on credit scoring. Use prepaid options. Use a credit reporting service like eCredable.

- Plan ahead: In some cases you may need to plan ahead in order to get what you want without using a credit. You may need to put down extra deposits, change a reservation to a hotel that accepts debit, or be ready to provide alternate proof of your creditworthiness. In some cases it may cost you more if you don’t have a credit history – like when getting a mortgage.

While living a debt and credit free lifestyle might not always be the easiest in today’s culture, it is still possible. Just realize that at times it may take a bit more legwork on your part. In the end, you’ll likely be glad you did because of the benefit of a simplified lifestyle, and no worries about debt hanging over your head.

What are your thoughts? Do you think you could live without credit? Would you want to?

For me, Yes it is possible to live without credit card. I am confuse on whether to get one soon. Great post.

Yes, it is possible to live without credit, and not having any credit card debt hanging over your head is definitely a load off your mind. If you’re confused about getting one soon, you may want to hold off! Having credit is like having a loaded gun – it can be used for positive purposes, but it can also be extremely dangerous if you don’t use it properly! Applicant beware!

I think I can live without a credit card. I always believe that having enough cash in your wallet and a debit card are better alternatives to a credit card.

cash and debit are definitely safer alternatives for most people, I can’t disagree with that!

Yes, it’s possible to live without a credit card, honestly, I don’t own one because my parents didn’t introduce it to me. They are not fan of credit card, I prefer to use cash instead.

Preferring to use cash is definitely not a bad thing.. I am in that same boat, and while I can understand why someone would want to use credit – it just isn’t something I plan on doing much of.

For the last couple of years I’ve been preaching that I don’t need credit. don’t want credit, and won’t ever use credit. I didn’t care about my credit score…..until i wanted to refinance my house. then I cared about my credit score. A LOT.

Yes, you CAN live without credit. But do you need to? You don’t have to ignore the game, you just have to be good a it. :)

I think you make a good point, it’s easy to not care about your credit, until caring about it makes your life a bit easier. We found the same thing when we were looking to get a new mortgage on our house. We had spent the last few years not really using credit in any way, but thankfully our credit score was still very good because we were making regular payments and were never late on our old mortgage. We had a ton of paperwork to get our mortgage. I can’t even imagine if we had to go through that by doing a manual underwriting because we had no credit score!