That’s right, Betterment is the original robo-advisor, as in first in the field.

But more importantly, it’s quite possibly the best.

You see, Betterment didn’t just lead the pack across the starting line, but they continue to improve their product in the 11 years they’ve been in operation.

If Betterment has a secret, it’s that they’ve committed to making investing simple and available to investors at all levels.

Even if you know absolutely nothing about investing – and have very little money – Betterment can help you get started. They provide everything you need, from creating your portfolio to providing a complete professional management going forward.

Whether you’re a brand-new investor looking to get started, or a seasoned investor looking for a low-cost managed option, Betterment is the robo-advisor to check out first.

Quick Summary

- The original robo-advisor.

- Very low advisory fee at 0.25% annually.

- Tax loss harvesting and value investing offered on all accounts.

- Low minimum investment ($0)

What is Betterment?

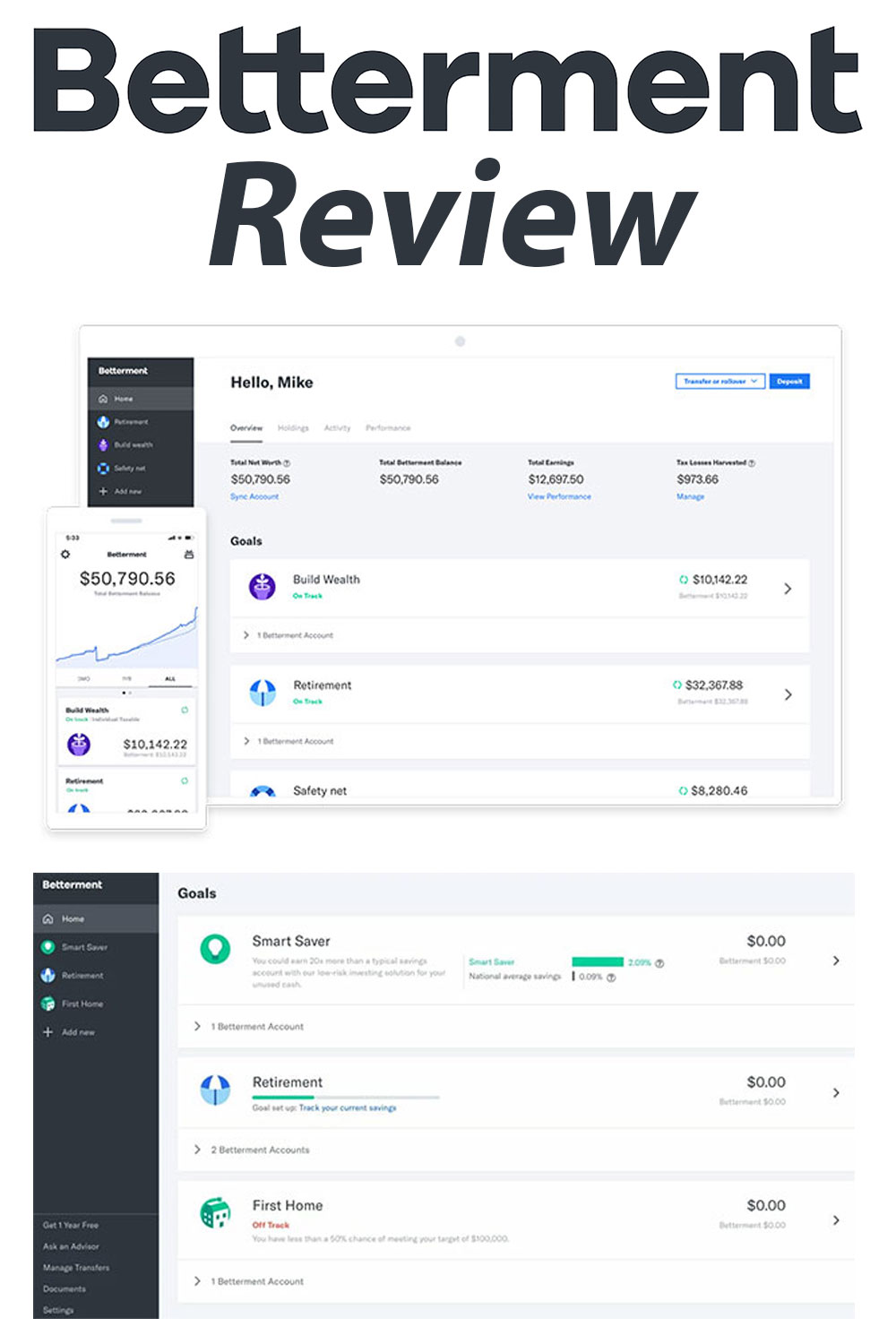

![]() Betterment is the first of a class of online, automated investment platforms that have become known as “robo-advisors”. “Robo” emphasizes the automated nature of their investment process. You, as the investor, don’t need to concern yourself with the details of your investment activities. All you need to do is fund your account, and Betterment handles all the details for you.

Betterment is the first of a class of online, automated investment platforms that have become known as “robo-advisors”. “Robo” emphasizes the automated nature of their investment process. You, as the investor, don’t need to concern yourself with the details of your investment activities. All you need to do is fund your account, and Betterment handles all the details for you.

With just a few hundred dollars, Betterment can construct a fully diversified portfolio, split between both stocks and bonds. And since they use exchange-traded funds (ETFs) to invest in more than a dozen asset classes, a small investment is spread across literally thousands of stocks and bonds. There’s no other way available to gain so much diversification with so little money.

Though Betterment only began operations in 2008, they have more than $16 billion in assets under management and have steadily remained the largest independent robo-advisor in the industry. In fact, the robo-advisor concept has become so popular that most major brokerage firms now offer their own version. Meanwhile, there have been dozens of other independent robos that have sprung up to compete with Betterment. Only a couple have come close, but Betterment continues to maintain the mojo of an industry leader.

Betterment has been steadily expanding its menu of product options, in addition to its primary menu of taxable investment and retirement accounts. They now offer portfolios dedicated to smart beta, socially responsible investing, and even fixed income-centered portfolios.

How Betterment Works

Like virtually all robo-advisors, Betterment uses an investment strategy known as Modern Portfolio Theory (MTP).

MPT emphasizes proper diversification through asset class selection, based on targeted investor risk levels.

It’s often referred to as a “passive” investment strategy, because it maintains asset class positions over the long-term, and avoids frequent trading. This is done by using ETFs, each of which represents a portfolio of securities tied to a specific common index for that asset class.

The S&P 500 index is a common index to represent the general US stock market. But there are other indexes that represent other asset classes, like international stocks, small-, medium- and large-capitalization stocks and various bond classes.

It’s a less expensive way to invest, since it avoids the need to buy and sell individual stocks and bonds.

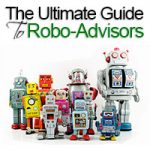

When you open an account with Betterment, you start by completing a questionnaire. The questions are designed to determine your investment goals, time horizon, and risk tolerance. Armed with that information, Betterment builds a portfolio designed to match your personal investor profile.

As a general rule, Betterment allocates your money between three different broad categories:

- Safety Net: This is money for more immediate needs in life.

- Retirement: Long-term savings, held in tax-sheltered plans, and dedicated to retirement.

- General Investing: Investing for medium-term goals, such as your children’s college educations, or just general investing for no particular purpose.

For example, I entered information for a 35-year-old with an annual income of $100,000. Here where the recommendations I received:

As you can see, the safety net portion is more conservatively invested. But both the retirement and general investing categories recommend 90% in stocks.

Once your portfolio has been created, Betterment will manage it through periodic rebalancing and reinvesting dividends.

Tax-loss harvesting

This is a feature Betterment provides on all taxable investment accounts (it’s not necessary on retirement accounts, since they’re tax-deferred). Tax-loss harvesting is a strategy in which losing asset positions are sold to create losses that offset gains in other asset classes.

In effect, tax-loss harvesting acts as a form of tax deferral for taxable accounts. Since losses reduce capital gains, those gains continue to roll forward without tax consequences. It doesn’t totally eliminate taxable gains, but it does reduce them, enabling you to retain more of your investment capital.

To maintain target asset allocations in your portfolio, the asset classes sold to generate losses are replaced with ETFs from the same asset class. This takes place at least 31 days later, to avoid triggering IRS wash sale rules.

As you’ll see a bit later in this review, Betterment works tax-loss harvesting by making use of two or more ETFs for each asset class. They can sell the current ETF, generate a loss, then replace that ETF with a comparable one to maintain the target asset allocation.

Once again, Betterment uses tax-loss harvesting with all taxable investment accounts. It doesn’t require a larger account balance, or additional advisory fees. Many other robo-advisors also use the strategy, but often require higher account balances.

Betterment Basic Features & Tools

Minimum initial investment: None! Betterment is one of only a handful of robo-advisors that allows you to open an account with no money at all. Of course, you’ll need to put funds into your account to begin investing. This can be done with regular deposits of, say, $100 per month. This makes Betterment the perfect platform for small or beginner investors, who may not have a large initial investment.

Available accounts: Individual and joint taxable accounts; traditional, Roth, rollover, and SEP IRAs; trusts and nonprofit accounts.

Mobile App: Betterment’s mobile app has all the capabilities of the online version. That means you can track your investments wherever you go, and at any time. The app is available at the App Store for iOS devices, 11.0 and later, and is compatible with iPhone, iPad, and iPod touch. It’s also available at Google Play for Android devices, 6.0 and up.

Mobile App: Betterment’s mobile app has all the capabilities of the online version. That means you can track your investments wherever you go, and at any time. The app is available at the App Store for iOS devices, 11.0 and later, and is compatible with iPhone, iPad, and iPod touch. It’s also available at Google Play for Android devices, 6.0 and up.

Customer service: Available by phone or email, Monday through Friday, 9:00 am to 6:00 pm, as well as Saturdays and Sundays, from 11:00 am. to 6:00 pm, all times Eastern. But be aware that customer service is available by email only on weekends.

Account protection: All Betterment accounts are protected by coverage from the Securities Investors Protection Corporation (SIPC) for up to $500,000 in cash and securities, including up to $250,000 in cash.

Account security: Your account can be set up with two-factor authentication. Even if a thief were to acquire your access codes, they’d be unable to enter your account due to the second authentication. This has become common practice with many financial providers, and requires the use of a unique verification code, emailed or texted to your smart phone device, to enter the account.

Betterment RetireGuide

Since so many investors use robo-advisors to manage retirement accounts, Betterment has set up this special service to help clients project their retirement needs. The RetireGuide feature is a tool designed for this purpose.

You’ll enter information on the RetireGuide screen, including your age, your household income, how much you already have saved for retirement, and how much you’re saving for retirement on an annual basis.

Armed with that information, RetireGuide will sync your external accounts, including your employer sponsored 401(k), 403(b) or other plans. It will track your progress on an ongoing basis, as well as make investment recommendations to help you meet your goal.

Betterment Financial Advice Packages

To help move beyond basic investment management, Betterment is also tiptoeing into the area of financial advice. The Financial Advice Package is an add-on benefit, that provides advice in very specific areas of financial planning. With each, you’ll get up to one hour of one-on-one advice from a dedicated financial expert.

Betterment is currently offering five financial advice packages:

- Getting Started Package, $199

- Financial Checkup Package, $299

- College Planning Package, $299

- Marriage Planning Package, $299

- Retirement Planning Package, $299

How Betterment Invests Your Money

All robo-advisors invest your portfolio in a mix of stocks and bonds, but the details can vary significantly from one robo-advisor to another.

Betterment invests in indexes of general categories of stocks and bonds. Those include both domestic and international stocks and bonds. Their portfolio mix is somewhat more limited than some other robo-advisors, who may also invest in natural resources, including gold and silver, and real estate investment trusts. Some even invest in more exotic assets, like cryptocurrencies.

Betterment’s investment philosophy is that by investing in the general markets, your portfolio is automatically invested in both real estate in natural resources. This is true, since many major publicly traded companies own significant real estate, and a number are also involved with natural resources.

But one area where Betterment departs from typical robo-advisor portfolios is that they devote a significant portion of each portfolio to value stocks. This is important because investing in value stocks has historically proven to be one of the most successful stock investing strategies. It’s one regularly employed by Warren Buffett, and other successful investors.

The basic idea is that you invest in stocks of companies that are overlooked by the general investment public. The companies are fundamentally strong, but they’re being ignored often because of past problems that have since been resolved, or because most investors are simply investing in other competitors. That means value stocks can be purchased at a discount relative to other companies in their industries.

Investing in value stocks gives you an opportunity to outperform the general market over the long-term. However, Betterment makes no claim to outperform the market, but only to match it. But the inclusion of value stocks adds that potential to the Betterment investment mix, which is something very few competitors offer.

Betterment Digital and Premium

Betterment offers two primary plans, Digital and Premium.

Betterment Digital Investment Program

Digital is their basic investment program, and has the lowest annual fees.

It comes with all the features we’ve discussed in this review so far, including tax-loss harvesting, and the ability to invest in both taxable and retirement accounts. Digital is available for account balances of any size.

Betterment Premium Investment Program

Betterment Premium includes all the features and benefits of the Digital plan, but also provides unlimited access to Betterment certified financial planners for guidance on life events. This service alone adds personal advice to what is generally an automated investment service. It gives you the best of both worlds – automated investing, and human advice.

The Premium plan also offers account syncing, which brings your other assets under the Betterment investment umbrella. It enables Betterment to provide management advice for those accounts as well. This includes employer-sponsored retirement plans, real estate you own, and even individual stocks.

The Premium plan requires a minimum account balance of $100,000 (excluding external accounts), and does come with a higher fee structure (see “Betterment Pricing” below).

The portfolio mix is the same for both Digital and Premium, and you can see the details in the next section.

External account syncing

Available only on Betterment Premium, external account syncing provides for a more holistic view of your entire financial situation.

Betterment doesn’t manage your external accounts, but it does provide advice on how to better manage them. For example, it can provide advice on asset allocation and use of lower-cost funds with your employer-sponsored retirement plan.

Betterment can also take your external investments into account in designing the accounts it actually manages. This will avoid duplication of investments within your overall financial position.

This is the type of service that’s available through traditional human investment advisors, but generally at fees ranging between 1% and 2% of your account balance. Betterment does essentially the same service, but at a fraction of the fee.

Where Betterment Invests Your Money – Digital and Premium Plans

Betterment divides your portfolio between 14 different asset classes, each represented by a single ETF. There are six stock asset classes, and eight bond asset classes. That asset mix is used whether you’re in the Digital or the Premium plans.

Don’t be concerned that there are more bond funds than stock funds. That’s not an indication that your portfolio will favor bonds. Betterment has simply determined that a larger number of bond classes is a preferred investment strategy. The split between stocks and bonds in your portfolio will be determined by your investor profile. If you’re determined to be an aggressive investor, that could mean 90% in stocks and 10% in bonds.

The specific asset classes, as well as the ETFs use for each, are included below. Notice that each of the stock classes uses three funds. One is a primary ETF, and the other two are alternates. This is part of the tax-loss harvesting strategy. The alternate ETFs are similar to the primary ETF, and will be used as replacement funds if and when the primary ETF is sold to take advantage of tax-loss harvesting.

Betterment makes less use of alternate ETFs in the bond classes. Only four of the classes have two or more funds, and four have no alternate funds at all. This is because tax-loss harvesting is less necessary with fixed income investments. It’s even more true with short-term bond funds, which are the primary asset classes making use of only one fund.

The allocations, and the investments in each, include:

Stocks:

- US Total Stock Market: Vanguard US Total Stock Market (VTI), Schwab US Broad Market ETF (SCHB), iShares S&P 1500 Index Fund (ITOT)

- US Value Stocks – Large Cap: Vanguard US Large-Cap Value (VTV), Schwab US Large Cap Value ETF (SCHV), iShares S&P 500 Value ETF (IVE)

- US Value Stocks – Mid Cap: Vanguard US Mid-Cap Value (VOE), iShares Russell Midcap Value Index (IWS), iShares S7P Mid-Cap 400 Value Index (IJJ)

- US Value Stocks – Small Cap: Vanguard US Small-Cap Value (VBR), iShares Russell 2000 Value Index (IWN), iShares S&P SmallCap 700 Value Index (IJS)

- International Developed Market Stocks: Vanguard FTSE Developed Markets (VEA), Schwab International Equity ETF (SCHF), iShares Tr/Core MSCI EAFE ETF (IEFA)

- International Emerging Market Stocks: Vanguard FTSE Emerging Markets (VWO), iShares Inc/Core MSCI Emerging (IEMG), Schwab Emerging Markets Equity ETF (SCHE)

Bonds:

- US High Quality Bonds: iShares Barclays Aggregate Bond Fund (AGG), Vanguard Total Bond Market ETF (BND)

- US Municipal Bonds: iShares National AMT-Free Muni Bond (MUB), SPDR Nuveen Barclays Capital Muni Bond (TFI)

- US Inflation-Protected Bonds: Vanguard Short-term Inflation Protected Securities (VTIP)

- US High-Yield Corporate Bonds: Xtrackers USD High Yield Corporate Bond (HYLB), SPDR Barclays Capital High Yield Bond (JNK), iShares iBoxx $ High Yid Corp Bond (HYG)

- US Short-term Treasury Bonds: iShares Barclays Short Treasury Bond (SHV)

- US Short-term Investment Grade Bonds: iShares Short Maturity Bond (NEAR)

- International Developed Market Bonds: Vanguard Total International Bond (BNDX)

- International Emerging Market Bonds: iShares Emerging Markets Bond (EMB), Vanguard Emerging Markets Government Bond (VWOB), PowerShares Emerging Markets PCY Debt (PCY)

Betterment’s Other Portfolio Options

The robo-advisor industry has been gradually expanding beyond managing a basic portfolio of stocks and bonds. More specialized portfolio options have been created, and Betterment offers perhaps a wider selection of alternatives than any other robo-advisor. This is hardly unusual, given Betterment’s status as an industry leader.

The different portfolio options offered include the following:

Socially Responsible Investing (SRI)

Socially responsible investing involves selecting companies that have been demonstrated to meet certain standards for social, environmental, and governance parameters. They advertise that the ETFs used in their socially responsible investing portfolio have generated 42% improvement in their social responsibility scores. This portfolio option is specially designed for those who prefer to invest in companies they believe in.

Socially responsible investing involves selecting companies that have been demonstrated to meet certain standards for social, environmental, and governance parameters. They advertise that the ETFs used in their socially responsible investing portfolio have generated 42% improvement in their social responsibility scores. This portfolio option is specially designed for those who prefer to invest in companies they believe in.

There is no minimum required investment for the socially responsible investing portfolio, and no additional fee.

The Socially Responsible Investing portfolio works similar to the basic Digital and Premium portfolios. It also uses 14 asset classes, except they’re evenly split at seven stock classes and seven bond classes. The specific asset classes for each are somewhat different from those offered on their regular portfolios. Once again, each is comprised of between one and three ETFs.

Just as is the case with Betterment’s other portfolios, the use of multiple ETFs enables the employment of tax-loss harvesting.

The ETFs included in Socially Responsible Investing Portfolio are as follows:

Stocks:

- US Socially Responsible Stocks – Large Cap: iShares MSCI KLD 400 Social ETF (DSI), iShares MSCI USA ESG Select ETF (SUSA)

- US Growth Stocks – Mid Cap: Vanguard Mid-Cap Growth ETF (VOT), Vanguard S&P Mid-Cap 400 Growth ETF (IVOG), iShares Russell Mid-Cap Growth ETF (IWP)

- US Growth Stocks – Small Cap: Vanguard Small-Cap Growth ETF (VBK), iShares Russell 2000 Growth ETF (IWO), Vanguard S&P Small-Cap 600 Growth ETF (VIOG)

- US Value Stocks – Mid Cap: Vanguard Mid-Cap Value ETF (VOE), iShares Russell Mid-Cap Value ETF (IWS), iShares S&P Mid-Cap 400 Value ETF (IJJ)

- US Value Stocks – Small Cap: Vanguard Small-Cap Value ETF (VBR), iShares Russell 2000 Value ETF (IWN), iShares S&P Small-Cap 600 Value ETF (IJS)

- International Developed Market Stocks: Vanguard FTSE Developed Markets ETF (VEA), Schwab International Equity ETF (SCHF), iShares Core MSCI EAFE ETF (IEFA)

- International Emerging Market Stocks: Vanguard FTSE Emerging Markets ETF (VWO), iShares Core MSCI Emerging Markets ETF (IEMG), Schwab Emerging Markets Equity ETF (SCHE)

Bonds:

- US High Quality Bonds: iShares Barclays Aggregate Bond Fund (AGG), Vanguard Total Bond Market ETF (BND)

- US Municipal Bonds: iShares National AMT-Free Muni Bond (MUB), SPDR Nuveen Barclays Capital Muni Bond (TFI)

- US Inflation-Protected Bonds: Vanguard Short-term Inflation Protected Securities (VTIP)

- International Developed Market Bonds: Vanguard Total International Bond (BNDX)

- International Emerging Market Bonds: iShares Emerging Markets Bond (EMB), Vanguard Emerging Markets Government Bond (VWOB), PowerShares Emerging Markets PCY Debt (PCY)

- US Investment-Grade Corporate Bonds: iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), Vanguard Intermediate-Term Corporate Bond Index Fund ETF Shares (VCIT), SPDR Portfolio Intermediate Term Corporate Bond ETF (ITR)

- US Short-term Treasury Bonds: iShares Barclays Short Treasury Bond (SHV)

Goldman Sachs Smart Beta

This is a highly specialized portfolio designed for investors with a minimum of $100,000 to invest, as well as a higher risk tolerance. That’s because it’s a high risk/high reward portfolio.

While it uses much of the same investment methodology as Betterment does, it modifies your portfolio to achieve higher results. It’s a more actively managed strategy, that specifically seeks to outperform the market.

The portfolio has 101 variations, ranging from 0% to 100% in stocks, depending on the investment objectives. Stocks are favored based on four major performance factors, including:

- Good value

- Strong momentum

- High quality

- Low volatility

Being actively managed, the portfolio will buy and sell securities. It invests in smart beta ETFs that are screened based on the four factors above. An attempt will be made to give greater weight in the investment mix to companies that are performing, or likely to perform, better than the total group of stocks in an asset class.

The normal fees that apply to a Betterment portfolio will also apply to the Smart Beta portfolio. No premium pricing is required

BlackRock Target Income Portfolio

Recognizing that some investors are primarily concerned with income, Betterment offers the BlackRock Target Income Portfolio. The portfolio seeks to maximize income, while minimizing loss of principal. It’s invested in bond ETFs, though there are four different portfolio levels – aggressive, high, moderate, and core (low). Each is offered based on your risk tolerance.

For example, the Moderate Income Model portfolio looks like this:

Flexible Portfolios

With this portfolio, Betterment gives investors some control over their investments. You can choose the individual investments held in your portfolio, but you can adjust the individual asset class weights. For example, if 10% of your portfolio is invested in a certain asset class, you can increase it to 15%. Alternatively, the 10% allocation can be reduced to 5%.

Even with the changes, Betterment will continue to automatically manage your portfolio. Once again, there is no additional fee for this option.

Tax-Coordinated Portfolio

This is less of a portfolio and more of an allocation strategy. Betterment allocates high tax investments to tax-sheltered retirement accounts. This may include holding interest or dividend bearing investments in an IRA. Meanwhile, capital gains generating assets, which have the benefit of lower long-term capital gains tax rates, may be held in a regular taxable account.

Betterment claims the strategy improves portfolio performance by an estimated 15% over 30 years.

Betterment Cash Reserve And Checking Accounts

Up until July of 2019 Betterment had an alternative to the high-yield savings products offered by online banks called Betterment Smart Saver. Your money was invested in very short-term securities that pay comparable rates to those offered on online savings accounts and CDs.

As of 7/23/19 Betterment announced the release of their new Betterment Cash Reserve account which will offer one of the highest APYs in the industry today.

How is it different from the Smart Saver product? It will offer a higher rate than most other savings accounts, have FDIC insurance up to $1,000,000, no minimum balance, no fees on balances and unlimited withdrawals (versus only 6 with most savings accounts).

The Checking account includes ATM fees reimbursed worldwide, no account fees, no overdraft fees, no minimum balance and FDIC insurance up to $250,000. It will also include a bright blue Betterment Visa debit card.

Betterment Pricing

As discussed earlier, Betterment offers two plans, based on the size of your portfolio. Digital is available for all account balances, while Premium requires a minimum balance of $100,000.

The basic fee structure that will apply to most investors is as follows:

The fees are reduced for portfolio balances that exceed $2 million or more under each plan. The reduced fee structure works like this:

- Digital plan: 0.25% on the first $2 million, then 0.15% on excess balances

- Premium plan: 0.40% on the first $2 million, then 0.30% on excess balances.

Each of the above represents a discount of 0.10% on the base rate.

Current Betterment Promotions

Betterment is offering free portfolio management for up to one year, based on the size of new deposits made into your account. The requirements are as follows:

- $15,000 to $99,999, one month free

- $100,000 to $249,999, six months free

- $250,000 or more, one year free

How to Sign Up with Betterment

As described earlier, when you open a Betterment account, you’ll be given a series of questions used to determine your investment goals, time horizon, and risk tolerance. You’ll start with the screen below:

You’ll then select your investment goals – Safety Net, Retirement or General Investing. A portfolio allocation will be recommended, which you will review and approve.

You’ll then provide your basic information, including contact information, verification of your identity, and relevant financial information, like employment status, annual household income, and estimated investable assets.

Certain regulatory questions will be asked to determine if you’re affiliated with a financial institution or you’re a major stockholder in a publicly traded company. You’ll set up account security, and then your account will have been created.

Funding Your Account and Making Withdrawals

You won’t need to immediately fund your account to open it. However, you will need to deposit funds to begin investing.

The best way to fund your account is by linking it to a checking account, and using automatic transfers. But you can also transfer assets from another brokerage account. Wire transfers can be used for larger amounts. Funds are automatically invested in one or two business days.

Unfortunately, Betterment does not accept funding by check, credit card or debit card.

The only way to make withdrawals is by electronic transfers into your checking account. Checks and wires are not available. Expect the withdrawals to take up to five business days to settle in your checking account.

Betterment Pros and Cons

Pros

Cons

Is Betterment Worth Signing Up For?

An investment platform like Betterment will work for investors at any level.

For the new or small investor, it’s an opportunity to gain professional management and a well-diversified portfolio with very little money.

For the more advanced investor, Betterment can provide a perfect managed investment option, alongside an otherwise self-directed investment strategy.

It’s also perfect for more experienced investors who may simply lack the time or the desire to do their own investing.

Betterment offers a very low basic annual advisory fee of just 0.25%. That means you can manage a $10,000 portfolio for just $25 per year, or $100,000 portfolio for just $250. It’s largely the same service you’ll get from traditional human investment advisors, but at a fraction of the cost.

If you’d like more information, or if you’d like to open an account, visit the Betterment website.

Betterment

Pros

- No minimum initial investment required

- Very low advisory fee

- Value investing offered on all accounts

- Tax-loss harvesting offered on taxable accounts

- Some control over your investments offered

Cons

- No alternative investments offered

- No FDIC coverage on Smart Saver account

{kind=link}

Share Your Thoughts: